Trump says Iran war "close to over" amid hopes for more negotiations

Introduction & Market Context

Companhia Brasileira De Distribuica (PCAR3) presented its third quarter 2025 results on November 5, highlighting operational improvements and a return to profitability. Despite the optimistic tone of the presentation, the company’s actual performance fell short of market expectations, with the stock declining 1.32% following the announcement.

The Brazilian retailer emphasized its growth in same-store sales and e-commerce while showcasing margin improvements. However, these positive narratives contrasted with the reality of missed revenue targets and earnings estimates that disappointed investors.

Quarterly Performance Highlights

GPA’s presentation emphasized several key operational achievements for the third quarter. Same-store sales increased by 4.1%, with Extra mercado stores growing by 5.5%, Pão de Açúcar by 3.5%, and proximity formats showing impressive growth of 17.3%.

The company also highlighted its leadership in food e-commerce, which now represents 13.1% of GPA’s total sales. E-commerce sales grew by 9.8% year-over-year with a Pre-IFRS 16 EBITDA margin of 10.3%.

As shown in the following highlights from the company’s presentation:

However, these operational metrics stand in contrast to the company’s overall financial performance. While the presentation emphasized a 4.1% increase in same-store sales, the earnings report revealed total sales growth of only 2.2% year-over-year. Additionally, the company’s revenue of 4.56 billion BRL missed analyst expectations of 4.74 billion BRL.

Detailed Financial Analysis

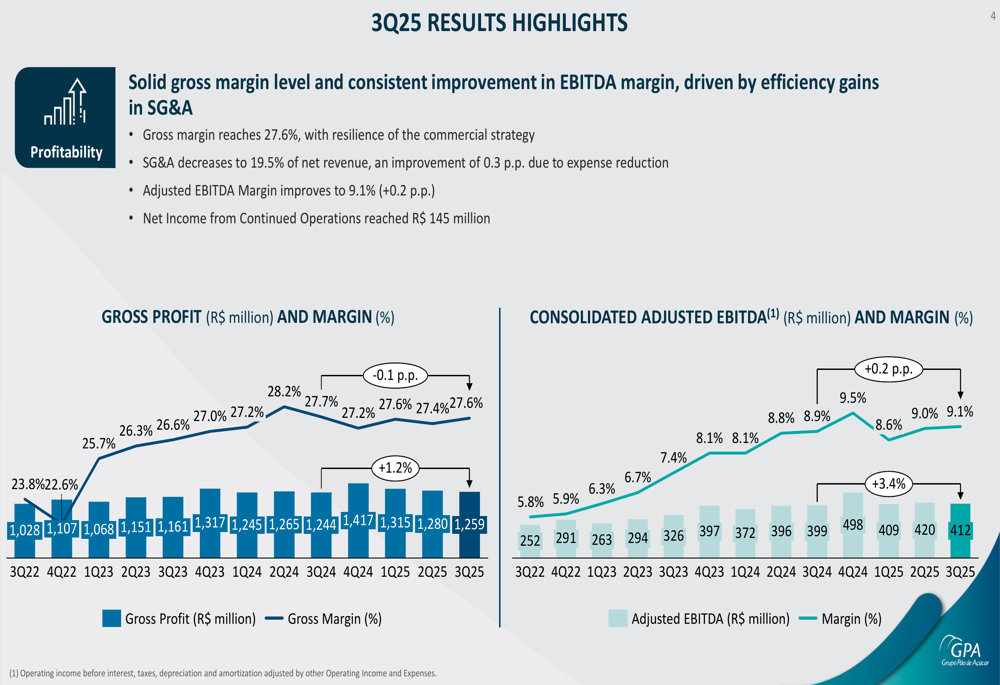

GPA’s presentation showcased improving profitability metrics, with gross margin reaching 27.6% in Q3 2025, a significant improvement from 23.8% in Q3 2022. Selling, general, and administrative expenses (SG&A) decreased to 19.5% of net revenue, an improvement of 0.3 percentage points. The adjusted EBITDA margin improved to 9.1%, representing a 0.2 percentage point increase.

The following chart from the presentation illustrates these profitability improvements:

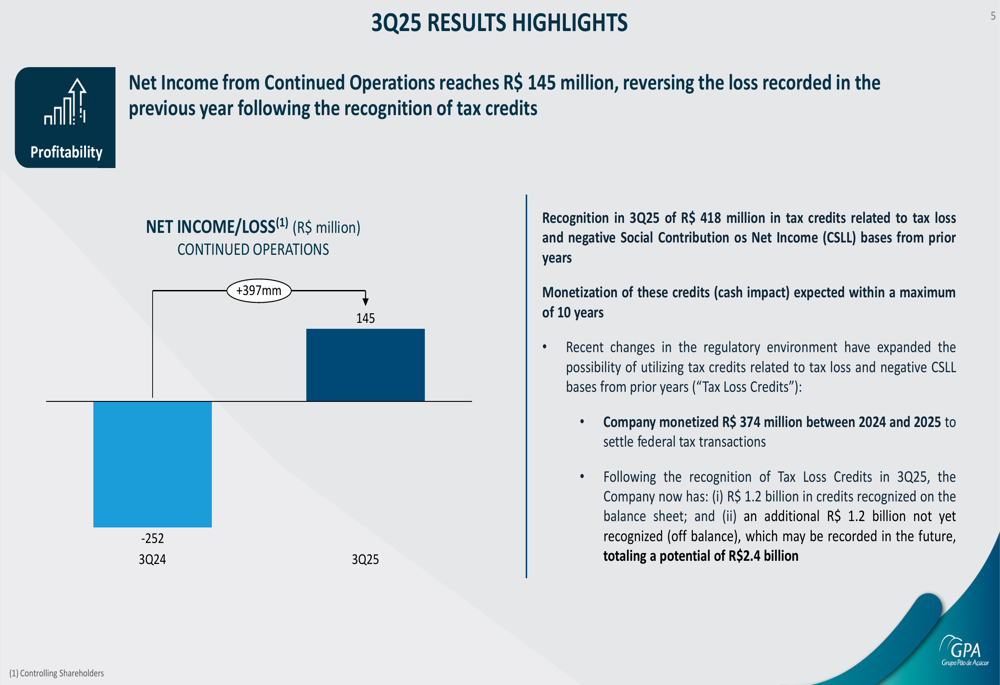

The most significant financial development was GPA’s reported net income from continued operations of R$145 million, which the company presented as a dramatic reversal from the previous year’s loss. This turnaround was largely attributed to the recognition of R$418 million in tax credits related to tax losses and negative Social Contribution on Net Income (CSLL) bases from prior years.

As shown in the following slide, these tax credits played a crucial role in the company’s return to profitability:

However, the earnings report revealed that GPA posted an EPS of -0.4827, missing the forecast of -0.4067 by 18.69%. This discrepancy suggests that the tax credit recognition, while improving the bottom line, masked underlying operational challenges.

Cash Flow and Financial Leverage

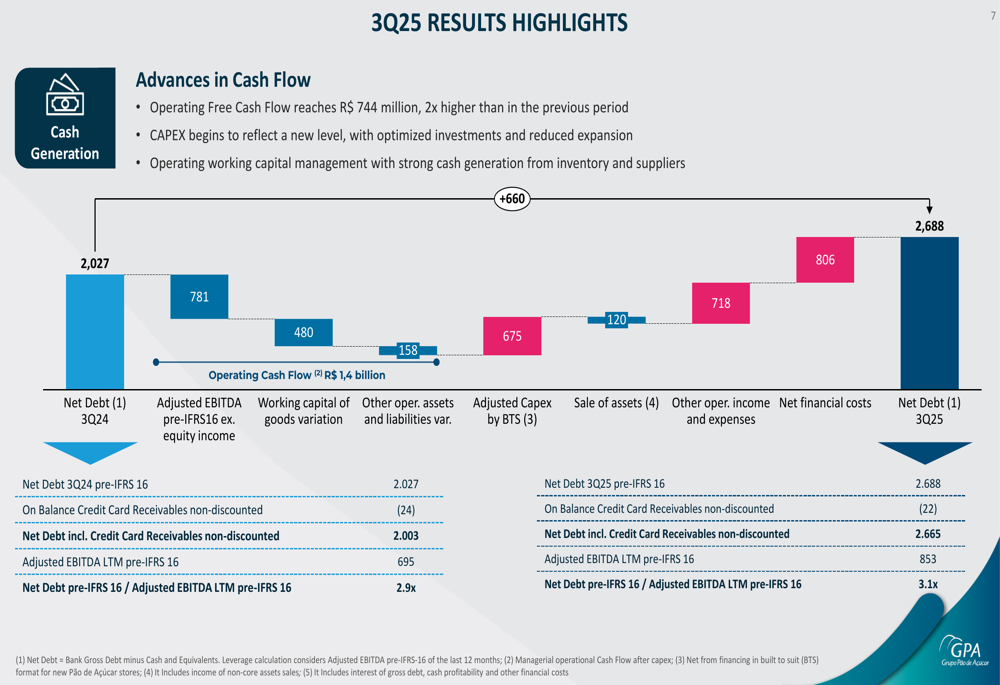

GPA emphasized its cash flow generation in the presentation, reporting that operating free cash flow reached R$744 million, twice the amount generated in the previous period. The company attributed this improvement to working capital management, particularly in inventory and supplier terms.

The following cash flow waterfall chart illustrates the company’s financial movements:

Despite the positive cash flow narrative, GPA’s net debt increased from R$2.027 billion in Q3 2024 to R$2.688 billion in Q3 2025. Consequently, the company’s leverage ratio (Net Debt/Adjusted EBITDA) deteriorated from 2.9x to 3.1x over the same period.

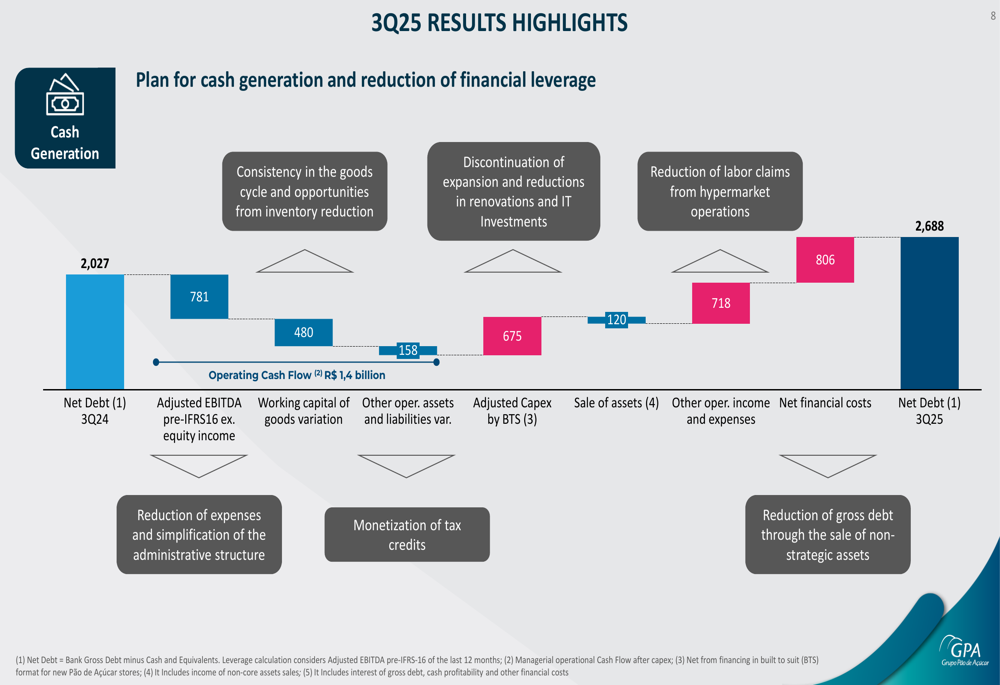

The company outlined its plan to address this increasing leverage through several initiatives:

These measures include optimizing the goods cycle, discontinuing expansion, reducing renovations and IT investments, decreasing labor claims, simplifying the administrative structure, monetizing tax credits, and selling non-strategic assets.

Strategic Initiatives

GPA’s presentation highlighted its strategic focus on premium and proximity segments, reporting a 0.6 percentage point gain in premium market share and a 1.6 percentage point expansion in proximity market share. The company also noted a 1.5 percentage point increase in share of wallet among loyal Pão de Açúcar customers.

The company’s e-commerce strategy appears to be gaining traction, with digital sales now representing 13.1% of total revenue. This positions GPA as a leader in food e-commerce in Brazil, providing a potential growth avenue amid challenging market conditions.

GPA also emphasized its commitment to sustainability through its ESG framework, which is built on four pillars: Respect for People, Respect for Food, Respect for the Environment, and Respect for Business.

Forward-Looking Statements

Looking ahead, GPA’s presentation focused on its plans for cash generation and debt reduction. The company aims to monetize its tax credits, with R$1.2 billion already recognized on the balance sheet and an additional R$1.2 billion not yet recognized, totaling a potential of R$2.4 billion.

The earnings report indicated that the company plans to reduce expenses by 450 million BRL in 2026 and maintain capital expenditures between 200-250 million BRL. These measures align with the cash generation and debt reduction strategy outlined in the presentation.

However, GPA faces significant challenges, including high interest rates, competitive pressures in the retail sector, and selective consumer behavior in a challenging macroeconomic environment. The company’s ability to execute its debt reduction plan while maintaining operational performance will be critical to regaining investor confidence after the disappointing Q3 results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.